Gig Workers and the Hidden Infrastructure of Credit Access

The Gig Worker Reality

Across emerging markets, millions survive by patching together income from multiple, irregular jobs. This is the reality for 59% of PayJoy customers, who are gig workers—drivers, delivery partners, micro-entrepreneurs, vendors, part-time workers, and those moving in and out of formal employment. These workers often clock long hours, yet still struggle with unpredictable income. For this population, the combination of irregular earnings, lack of financial safety nets, and dependence on smartphones for work creates a cycle of vulnerability.

PayJoy’s latest report,Gig Workers and the Hidden Infrastructure of Credit Access, highlights the critical role of PayJoy’s secured-credit model in directly addressing this gap.

Credit as the Safety Cushion

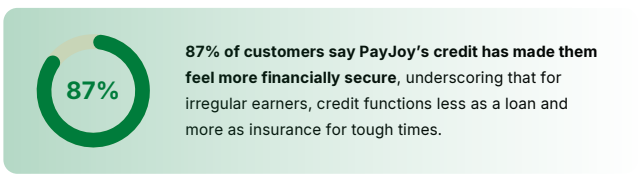

Traditional financial systems typically exclude gig workers, leaving them with few safe options when income gaps emerge. UC Berkeley research shows that access to a PayJoy loan is equivalent to a 6% increase in income for the average customer—a meaningful gain for households operating on razor-thin margins. Critically, 87% of customers say PayJoy’s credit has made them feel more financially secure, underscoring that for irregular earners, credit functions less as a one-off loan and more as insurance for tough times.

Smartphones as Essential Infrastructure

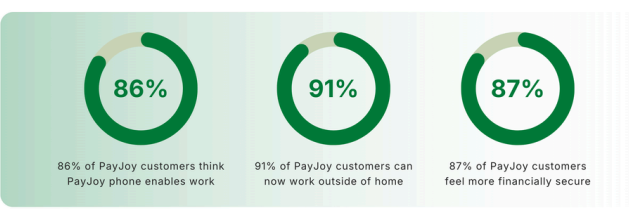

For gig workers, the smartphone is the workspace, marketplace, and payment terminal. Among PayJoy customers, 86% say their PayJoy-financed phone enables them to work in their current job or business, and 52% report that it has increased their income. 91% say their phone lets them work outside the home, and 87% say it enables them to work at home, providing crucial flexibility for caregiving demands, transportation constraints, and multiple job schedules.

Building Pathways Out of Fragility

Each on-time payment builds a digital credit trail, allowing customers to qualify for better financial products over time. Research shows that access to credit can reduce the risk of extreme poverty by 25% and can double households’ spending on education. For previously excluded gig workers, this “graduation effect” turns basic device finance into a first rung on the ladder of financial inclusion

Explore Similar Journeys.

.webp)

From Innovation to Impact: PayJoy's Financial Evolution